Understanding Medicare in Kansas

Table of Contents

Medicare is the federal health insurance program in the United States, available to eligible Kansas residents and administered by the Centers for Medicare and Medicaid Services (CMS). It provides health insurance coverage to people who are 65 years of age or older, as well as to some younger people with disabilities or end-stage renal disease (ESRD). Established in 1965 as part of the Social Security Act, Medicare has grown into one of the nation's largest health insurance programs, covering more than 65 million Americans — including hundreds of thousands of Kansas residents.

Is Medicare state or federal? Medicare is a federal program, not a state one. The rules, benefits, and eligibility are set at the national level by CMS, so Kansas residents get the same core Medicare coverage as everyone else in the country. What varies by state (and even by zip code) are the private plans that layer on top — Medicare Advantage (Part C), Part D drug plans, and Medigap policies.

Understanding how Medicare works is essential whether you are a KS resident approaching 65, helping a loved one navigate their options, or simply planning ahead. This guide breaks down the four parts of Medicare, who qualifies, how to enroll, what it costs, and how to decide which plan is right for you.

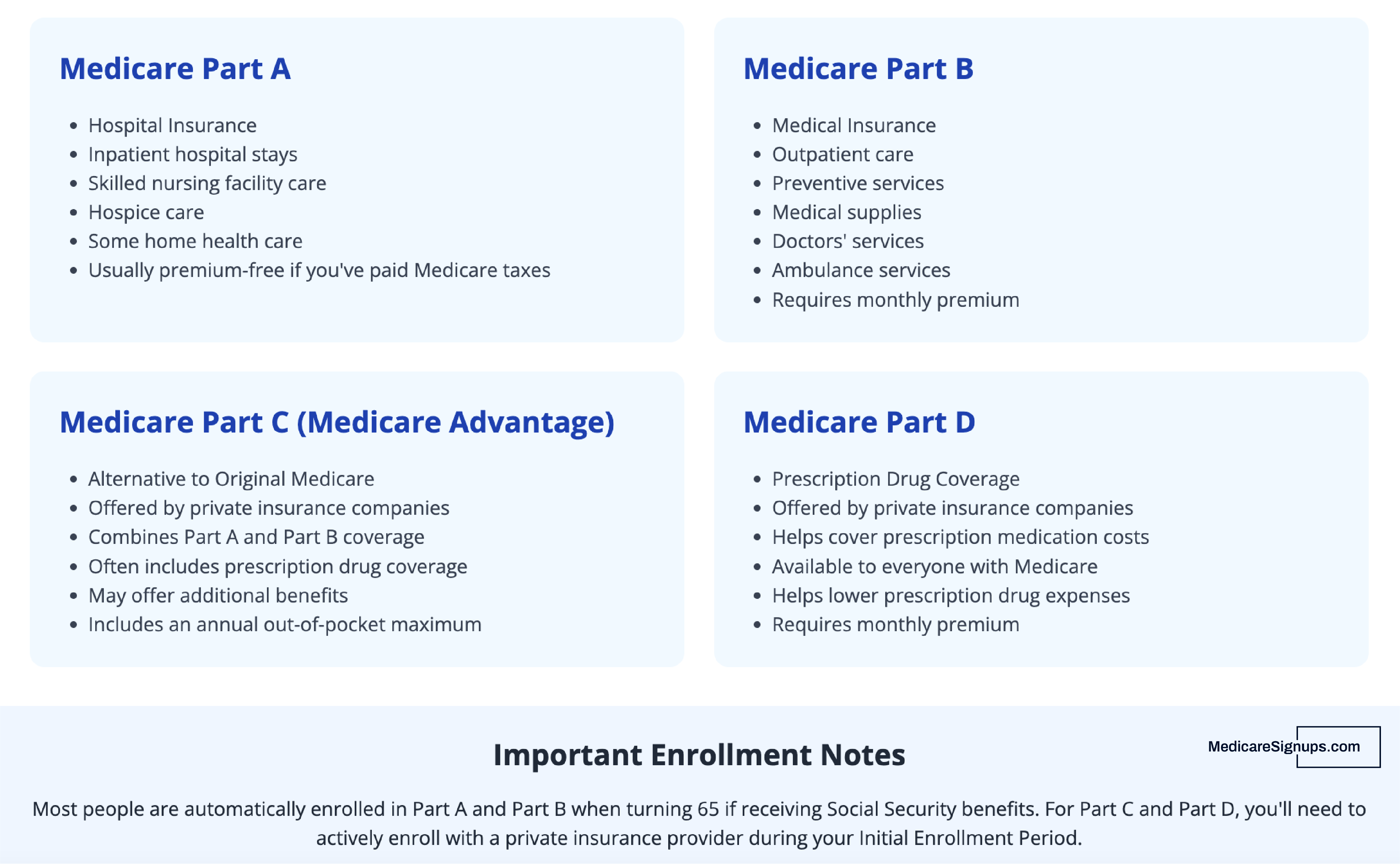

The Four Parts of Medicare

Medicare is divided into four distinct parts, each covering different services. Together, they form a comprehensive framework for healthcare coverage available to Kansas residents.

Medicare Part A: Hospital Insurance

Medicare Part A covers inpatient hospital stays, skilled nursing facility care, hospice care, and some home health services. Most Kansas residents do not pay a monthly premium for Part A because they or a spouse paid Medicare taxes for at least 40 quarters (10 years) during their working years. However, Part A does come with a deductible — $1,676 per benefit period in 2025 — and coinsurance charges apply for longer hospital stays.

Medicare Part B: Medical Insurance

Part B covers medically necessary services like doctor visits, outpatient procedures, preventive screenings, durable medical equipment, and mental health services. The standard Part B premium in 2025 is $185 per month, though higher earners pay more through Income-Related Monthly Adjustment Amounts (IRMAA). Part B also carries an annual deductible of $257 and typically requires a 20% coinsurance on most services after the deductible is met.

Medicare Part C: Medicare Advantage Plans in Kansas

Medicare Advantage (Part C) is an alternative way to receive your Medicare benefits through private insurance companies approved by Medicare. These plans bundle Part A and Part B coverage — and most include Part D prescription drug coverage as well. Many Medicare Advantage plans available to Kansas residents offer additional benefits not available through Original Medicare, such as routine dental, vision, and hearing care. Plan types include HMOs, PPOs, and Special Needs Plans. One significant advantage is that Part C plans include an annual out-of-pocket maximum, which Original Medicare does not.

Medicare Part D: Prescription Drug Coverage

Medicare Part D provides coverage for prescription medications, including brand-name drugs, generics, and vaccines. Part D plans are offered by private insurers and each plan has its own formulary — a list of covered drugs organized into tiers that determine your cost-sharing. If you do not enroll in Part D when you are first eligible and lack other creditable drug coverage, you may face a late enrollment penalty that increases your premiums permanently. The penalty is calculated as 1% of the national base beneficiary premium for every month you went without creditable coverage, added to your Part D premium for as long as you have the plan. Kansas residents should compare Part D plans carefully since formularies and costs can vary significantly by zip code.

Medicare Eligibility in Kansas: Who Qualifies

You are eligible for Medicare if you meet one of the following criteria:

- Age 65 or older and a U.S. citizen or permanent legal resident who has lived in the United States for at least five continuous years

- Under 65 with a qualifying disability — you become eligible after receiving Social Security Disability Insurance (SSDI) for 24 months. Learn more about how to qualify for Medicare under 65.

- End-Stage Renal Disease (ESRD) — permanent kidney failure requiring dialysis or a transplant qualifies you regardless of age

- Amyotrophic Lateral Sclerosis (ALS) — Medicare coverage begins the same month your SSDI benefits start, with no waiting period

Most Kansas residents who are already receiving Social Security benefits are automatically enrolled in Medicare Parts A and B when they turn 65. If you are not collecting Social Security, you will need to actively sign up.

"Many people sign up for Part A even if they are continuing to work, since it is a benefit they have earned and does not cost anything extra," says Michelle Sparks, a licensed Medicare agent in Kansas. "If you are still working at age 65 and covered by a creditable employer group health plan, you can hold off on Part B without a late enrollment penalty — just ask your HR department to confirm your coverage is creditable before you skip Part B."

How Medicare Works in Kansas: Enrollment Periods & How to Sign Up

Here is how Medicare works when it is time to sign up. There are several key enrollment periods KS residents should know:

- Initial Enrollment Period (IEP): A seven-month window that begins three months before the month you turn 65, includes your birthday month, and extends three months after. This is your primary opportunity to enroll without penalties.

- General Enrollment Period (GEP): Runs from January 1 through March 31 each year for people who missed their IEP. Coverage begins the first day of the month after you enroll, and late enrollment penalties may apply.

- Special Enrollment Periods (SEPs): Triggered by qualifying life events, such as losing employer coverage, moving to a new area, or other circumstances that allow you to enroll or make changes outside the standard windows. Learn more about who qualifies for a Medicare SEP.

- Annual Enrollment Period (AEP): Runs from October 15 through December 7 each year, allowing you to switch between Original Medicare and Medicare Advantage or change your Part D plan.

You can apply for Medicare online at ssa.gov/medicare, by calling Social Security, or by visiting your local Social Security office in Kansas.

"Just because you are continuing to work and keep your insurance doesn't mean that it's the better option compared to going on to Medicare," says Cody Brown, a licensed Medicare agent in Missouri. "Sometimes Medicare beats most employer-provided insurances — lower premium, less out-of-pocket. It's a good idea to keep Part A, but you can delay your Part B for however long you want as long as you keep that creditable insurance through your employer. You don't have to pay any penalties down the road whenever you decide to get on Medicare."

Medicare Costs: What Kansas Residents Should Expect

Medicare is not free. While many people pay no premium for Part A, other costs include:

- Part A deductible: $1,676 per benefit period (2025)

- Part B premium: $185/month standard; higher for incomes above $106,000 (single) or $212,000 (married filing jointly)

- Part B deductible: $257/year

- Part B coinsurance: Typically 20% of the Medicare-approved amount for most services

- Part D premiums: Vary by plan, averaging around $46/month nationally

- Medicare Advantage premiums: Many plans have $0 additional premiums beyond your Part B premium, while others charge a monthly fee for enhanced benefits

For Kansas beneficiaries with limited income, Medicare Savings Programs and Extra Help (Low-Income Subsidy) can reduce or eliminate many of these costs. If you qualify for both Medicare and Medicaid, understanding how dual eligibility works can help you maximize your benefits. Be aware that missing enrollment deadlines can result in permanent late enrollment penalties.

According to Voss Speros, a licensed Medicare agent in Arizona, "If you're just enrolled in A and B, you're covered — but that's an 80/20. Medicare covers 80% of your healthcare, and you're responsible for 20%. And you don't have a drug plan either. If later in life you need help with drugs and want to add a Part D plan, you'll have a lifetime penalty for not taking it back when you first got Part A and B."

Original Medicare vs. Medicare Advantage in Kansas

One of the biggest decisions KS residents face is choosing between Original Medicare and a Medicare Advantage plan. Here is how they compare:

Original Medicare (Parts A and B) is administered directly by the federal government. You can see any doctor or hospital in Kansas — or anywhere in the country — that accepts Medicare, with no referrals needed and no network restrictions. However, Original Medicare does not cap your out-of-pocket spending, which is why many beneficiaries add a Medicare Supplement (Medigap) plan to cover deductibles, coinsurance, and copays. You will also need a separate Part D plan for prescription drug coverage.

Medicare Advantage (Part C) bundles your benefits through a private insurer. Most plans include prescription drug coverage, and many add dental, vision, hearing, and wellness benefits. The tradeoff is that you typically must use in-network providers in Kansas and may need referrals to see specialists. The key upside is a built-in annual out-of-pocket maximum, which provides financial predictability that Original Medicare lacks. Learn more about the benefits driving seniors to Medicare Advantage.

"I don't recommend that anyone just have Part A and B alone. There are significant gaps in coverage, and no maximum out-of-pocket cost," says Casey Ahlbum, a licensed Medicare agent in Florida. "Adding a supplement can be the best approach to cover those gaps — the premiums are predictable, and your retirement savings is protected."

"Medicare Advantage can also limit out-of-pocket costs and will cost less in the short term, but it's managed care: you stay within a network, they can require referrals and pre-approvals, and you'll pay cost-sharing up to a maximum out-of-pocket limit that typically runs $5,000 to $7,000 in-network," Ahlbum adds.

How to Choose the Right Medicare Plan

Selecting the right plan depends on your individual circumstances. Consider these factors as a Kansas resident:

- Your health needs: Do you have chronic conditions that require specialist care? Do you take multiple prescription medications?

- Your preferred doctors: Are your Kansas doctors in-network for the Medicare Advantage plans you are considering, or would you prefer the flexibility of Original Medicare?

- Your budget: Compare total annual costs — not just premiums, but deductibles, copays, and coinsurance.

- Travel: If you spend time in multiple states, Original Medicare's nationwide acceptance may be more practical than a regional Medicare Advantage network.

- Prescription drugs: Review the formularies of Part D or Medicare Advantage plans to confirm your medications are covered at a reasonable tier.

"If you travel often, the type of plan really matters," says Leslie Kaz, a licensed Medicare agent in California. "Original Medicare with a Medigap plan lets you see any doctor or hospital in the U.S. that accepts Medicare, and many Medigap plans like Plan G and Plan N include limited foreign travel emergency coverage. Medicare Advantage HMO plans usually only cover you in-network, except for emergencies or urgent care while traveling."

A local Medicare insurance agent in Kansas can help you compare options at no cost — agents are compensated by insurance companies, not by you.

Common Medicare Misconceptions

Several myths about Medicare can lead to costly mistakes:

- Medicare is completely free. While Part A is premium-free for most people, Part B, Part D, and supplemental coverage all carry costs.

- Medicare covers everything. Long-term custodial care, most dental and vision services, and care outside the U.S. are generally not covered under Original Medicare.

- You can enroll anytime. Missing your enrollment windows can result in permanent late enrollment penalties and gaps in coverage.

- All Medicare plans are the same. Plans vary significantly in cost, coverage, and provider networks. Comparing options is critical.

The Bottom Line

Medicare is a foundational health insurance program that serves millions of Americans, including Kansas residents who depend on it for affordable healthcare coverage. Understanding its four parts, eligibility rules, enrollment windows, and costs empowers you to make informed decisions. Whether you choose Original Medicare with a supplement or a Medicare Advantage plan, the right choice depends on your health needs, financial situation, and personal preferences. If you are new to Medicare, take the time to research your options — the decisions you make now will affect your coverage and costs for years to come.

Matt Temmen

Licensed Kansas Medicare Agent

Contact Matt through Medicare Agents Hub »

Hello, my name is Matt Temmen. I have personally helped over 1,300 people with their transition to starting Medicare. I get it, it's overwhelming, confusing and you just want it done. You just don't want to make a mistake along the way. That's where I can help! We make the entire process easy by helping you apply for Medicare, compare Medicare Advantage vs Supplement and then going through your drug costs.

If you're already on Medicare we can help lower your Medicare Supplement rate or help you find a more beneficial Medicare Advantage plan. Overall anyone can sign you up and never answer the phone when you need help. We help you along the way and every single year we will do a check up with you to make sure you're in the right spot for the upcoming year.

Talk soon!